QUESTION BANK WITH ANSWER - GROUP ‘B’ AMM ( Stores) Part IV

Descriptive Questions:

Descriptive Questions:

238. From which different sources stores are received in a depot, please describe in detail.

Ans. Stores are received in a depot through the following sources:-

Ans. Stores are received in a depot through the following sources:-

(i) Against Purchase:

(a) Indigenous purchases- In case the original receipt and inspection of stores from the firms are centralized in one station, the inspecting and receiving Officer will issue the Receipt Note (S, 726) and forward the relevant foils to the stores depot concerned. In other cases, the Receipt Section of the depot receiving the material from the firm will issue the necessary Receipt note (S. 719 or S. 726). In certain cases as when stores are obtained from the National Instruments (Private) ltd,, or the Controller of Printing and Stationery, the supplies will be supported by the forms of the department making the supply.

(b) Imports.- Such stores will be supported by Advices of Despatch (S. 948) prepared by officer landing the stores.

(ii) Manufactures from Workshops.- The workshops send the materials under “Material supplied to Stores Form” (S. 1531).

(iii) Returned Stores.- These will be received on Advice Notes of Returned Stores (S. 1539) from the several departments of the Railway.

(iv) Depot Transfers.- These will be received on the special issue notes (S.1320) for such transactions.

(v) Sale/Loan of stores from other railways, etc.

(vi) Materials sent by departments to depot attached to workshops, not for stock, but for transmission to the workshops for repair & c.

(vii) Sample received from firms.

(vii) Sample received from firms.

(viii) Returnable empties (optionally or otherwise).

Q.239.What is unit piling? Explain.

Ans. Unit Piling.- In order to enable the compact stocking of material and to allow of the existing stock at any time to be ascertained at a glance, a system of stocking the stores so many deep to a row and so many rows to a layer of the stores, or in cases of small items, s system of packing in bags uniform quantities of items in convenient weights or number based on average quantities for one issue should be adopted, In addition, wherever practicable, graduation makers should be painted on bins to show certain previously ascertained quantities which would enable a busy depot store-keeper, incharge of materials to know at a glance the approximate stocks in his custody and assist him in taking steps prompt recoupment.

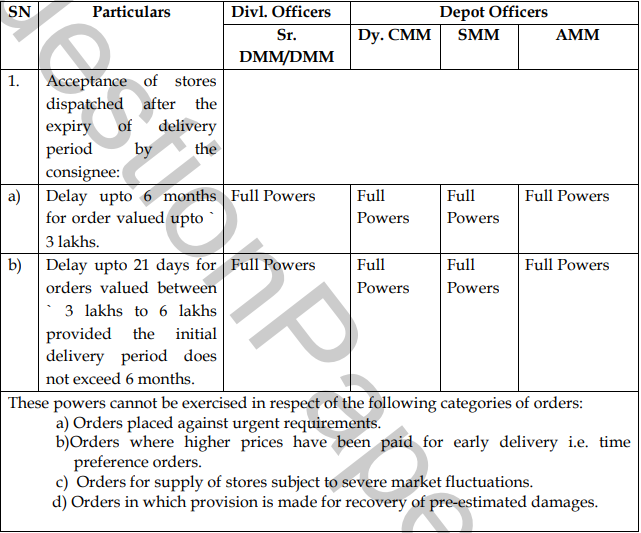

Q.240.Are depot officers empowered to accept stores dispatched by the supplier after the expiry of delivery period of the purchase orders placed by COS office ? Is there any value and time limit for such cases and what are the exceptions of POs where such powers can not be exercised?

Ans. Powers to depot officers to accept the stores dispatched by the supplier after the expiry of delivery period of the purchase orders placed by COS office are as below:

Q.241.What are the different categories of items for deciding the agencies for vender approval, vender development & inspection of the items? Explain in detail.

Ans. Categories of items:- As per the directives of the Board issued vide letter number 99/RS(G)709/1Pt.I dated 11.03.05, the different categories are defined as under:

(i) For category-III items, PUs are also permitted to develop new sources. In all such cases the first inspection of the bulk procurement must be carried out by RDSO and after final approval of the vendor on successful completion of the first bulk order, the vendor be incorporated in RDSO’s approved vendor list without any need for reassessment by RDSO.

(ii) In case of Loco items, the PUs may develop and register vendors which are essential to continue the ongoing indigenization programme for the locomotives.

Q.242.What are the duties of Depot Material Superintend?

Ans. Duties of Depot Material Superintend:- Depending on the section he is placed incharge of, the Depot Material Superintend shall be responsible for the discharge of the relevant items among the list of duties shown below :

Ans. Duties of Depot Material Superintend:- Depending on the section he is placed incharge of, the Depot Material Superintend shall be responsible for the discharge of the relevant items among the list of duties shown below :

(a) All correspondence by wards with departments will pass through the Depot Material Superintend, who will put them up to the Depot Officer, if necessary.

(b) The Depot Material Superintend will deal with all correspondence regarding stock verification reports.

(c) He will check recoupments, figures of consumption, and maxima and minima shown on stock cards (S. 1402).

(d) He will attend to complaints regarding shortages and delay in supplies, and bring all serious complaints to the notice of the Depot Officer.

(e) He will see that every convenience is placed at the disposal of the Accounts Stock Verifier for accurate and speedy verification of stocks and that store department witnesses attend and vary out their functions properly.

(f) He will check the figures of stock and consumption shown by wards on Annual Contract Statements (S.603).

(g) He will make surprise checks of packages by opening them and comparing the contents with the corresponding issue notes, and will initial the record copy of the issue notes so checked.

(h) He will supervise generally that material is properly handed over to the Dispatch Section, and that material is properly packed, whether packed by the ward or the Dispatch section.

(i) He will maintain general supervision over the wards, and see that material is properly stocked and looked after and kept in the correct bins and shelves.

(j) He will have under his direct control the registration of requisitions and their distribution to wards. (k) He will allot the duties of the clerical relieving staff of the depot.

(l) He will see that shunting operations are properly carried out in the yard, and that wagons are put in their proper places and to time.

(m) He will maintain an Inward and Outward Wagon Register (S.1215).

(n) He will personally check, with the Wagon Registers, the Authority for removal of wagons and the Weekly statement sent by the Traffic Department of the wagons sent to, and received from, the Yard. In the event of any discrepancy, he will immediately report it to the Depot Officer, for investigation. (o) He will pay surprise visits at night to the stores yard, and see that the chowkidari staff are alert and at their posts.

(p) He will maintain an inventory of all articles of dead stock, viz., plant, machinery, furniture, tools, instruments etc., at each depot in Inventory Books (S. 2001) maintained separately for each depot.

(q) He will prepare indents for consumable stores and tools and plant required by the depots, and will put them up to the Depot Officer for signature.

(r) He will arrange to test all weigh-bridges and weighing machines in the store yards and wards once in a month in the first week of the month. He will record the results of the check in a manuscript register (S. 1209) to be maintained specially for the purpose and will put it up to the Depot Officer whenever the results of test show any appreciable difference. Where there is no Depot Material Superintend of the lower grade, the Depot Material Superintend will in addition be responsible for: (s) The control and supervision of all labour and chowkidari staff, if provided instead of RPF staff, including a surprise roll call of all such staff at least once a weak.

(t) The correct preparation of Labour Muster Rolls.

(u) Witnessing the payment of labour staff and chowkidars.

(v) Seeing that the Yard is kept tidy, and reporting when necessary, on the state of roads, sidings, building & c,

(w) Seeing that the fire arrangements are kept up-to-date and that fire drills are held at least once a month.

(x) Preparing requisitions for repairs to material either by railway workshops or outside firms.

Q.243.Explain the procedure for accountal of materials received without documents:

Ans. Materials received without Documents.- Whenever any material is received without the accompanying documents, the Yard Foreman should enter all relevant details in the Wagon Register (S.1215) and immediately report such cases with full details to the Receipt Section and obtain the papers, if they are in that section. If they have not been received from the parties concerned the Receipt Section should enter such cases with full particulars, as far as available, from the Railway Receipts in a manuscript register (S. 1217) and if the documents are not received within three days from the receipt of the material, a letter should be addressed to the party concerned calling for the documents, copy of such letters being sent to his immediate superiors and district of divisional officer. The cases should be pursued till the documents are received and the stores are properly disposed off or if there is delay of over a month or if material is to be issued urgently or the party sending the material cannot be traced, the stores should be taken into stock by credit to stock Adjustment account.

Q.244. In how many copies Receipt Order is prepared? What is the distribution of the copies of Receipt Order?

Ans. Receipt Order is prepared in 4 copies. First copy of the Receipt Order is kept for the record of Receipt Section of the depot, Second Copy is kept by the stocking ward of the depot, Third copy is forwarded to FA&CAO office and fourth copy which is pink in color is sent to the supplier.

Q.245. Describe the R.O. number scheme in detail.

Ans. R. O. No (Reciept Order No.)- A 9 digit coding structure is adopted as shown below: Structure Position; : XX XXXX XX X Type of R. O. Serial Month in Last digit of Receipt Number two digits the year

i). Codes for type of receipt:

Type of Receipt Stock Non-stock

Type of Receipt Stock Non-stock

* COS Purchase for the depot 01 51

* Transit depot where the material is inspected but is 02 52

meant for other depot

meant for other depot

* DGS&D purchase, including RC/RGC 03 53

* Imported 04 54

* Railway Board contract 05 55

* Other Railways 06 56

* Imprest R. Os/Petty Purchases 07 57

* Fabrication orders 08 58

* Fabrication orders 08 58

ii). Four digit consecutive serial number is to be adopted sequentially to be changed once in a year or when the block reaches the maximum.

Q.246.What is ASRS? Explain the working of ASRS and how it can be beneficial to use in a Stores depot. Ans. hindi

Q.247. How the inventory turnover Ratio is calculated?Inventory opening balance of a depot was ` 2.5 Crore. Receipt from various supplies during the year was ` 10 Crore, and materials worth ` 0.75 Crores were collected from other depots on depot transfer. Materials worth ` 10 Crores were issued by the depot during the year to various users, and materials worth ` 1.25 Crore were transferred to other depots on depot transfer. Calculate percentage inventory tune over ratio for this depot at the end of the year.

Ans. Inventory Closing Balance Inventory Turn Over Ratio = ------------------------------------ x 100

Total Issue during the year Opening Balance = 2.5 Cr. Receipt

= (10Cr. + 0.75 Cr. – 1.25 Cr.)

= 9.5 Cr. Issue = 10 Cr. Closing Balance = (2.5 + 9.5 -10)

= 2 Cr. 2 T.O.R. = ------------- x 100 = 20 % 10

Ans. Inventory Closing Balance Inventory Turn Over Ratio = ------------------------------------ x 100

Total Issue during the year Opening Balance = 2.5 Cr. Receipt

= (10Cr. + 0.75 Cr. – 1.25 Cr.)

= 9.5 Cr. Issue = 10 Cr. Closing Balance = (2.5 + 9.5 -10)

= 2 Cr. 2 T.O.R. = ------------- x 100 = 20 % 10

Q.248. What are the parameters to be considered in designing a Model Stores Depot?

Ans. A good lay out aims at the following:

- Maximum utilization of available space providing for safety and security.

- Less material handling. - Better facilities for inspection.

- Avoid congestion and achieve greater efficiency of the stores depot.

- Avoid multiple handing of the material. - Facilitate to strictly observe ‘First-in-First-out’ procedure. - Better utilization of equipment and man power.

-Building factor, including the security aspect against fire, theft and pilferage.

- Man power factor,

- Service factor & Flexibility factor. In addition, the following aspects also should be considered.

- Flow of material should be simple and unidirectional, as far as possible.

- Scope for future expansion.

-Office accommodation, approach roads, separate Godowns / enclusures for oil, oxygen, paint, timber, Acids, chemicals and strong rooms for precious, pilfergable, non-ferrous items etc.

- Construction of sump for fire fighting hydrants with approach road facilities, fire extinguishers, etc. - Compound wall of sufficient height.

- There should be one main gate (for road) with one rail gate (Rail connectivity) for allowing wagons to be placed inside the depot.

-Lighting in the yard, inside godowns and along the compound wall and provision of tower lights/watch towers. -Provisioning of handling equipments.

- Maximum utilization of available space providing for safety and security.

- Less material handling. - Better facilities for inspection.

- Avoid congestion and achieve greater efficiency of the stores depot.

- Avoid multiple handing of the material. - Facilitate to strictly observe ‘First-in-First-out’ procedure. - Better utilization of equipment and man power.

-Building factor, including the security aspect against fire, theft and pilferage.

- Man power factor,

- Service factor & Flexibility factor. In addition, the following aspects also should be considered.

- Flow of material should be simple and unidirectional, as far as possible.

- Scope for future expansion.

-Office accommodation, approach roads, separate Godowns / enclusures for oil, oxygen, paint, timber, Acids, chemicals and strong rooms for precious, pilfergable, non-ferrous items etc.

- Construction of sump for fire fighting hydrants with approach road facilities, fire extinguishers, etc. - Compound wall of sufficient height.

- There should be one main gate (for road) with one rail gate (Rail connectivity) for allowing wagons to be placed inside the depot.

-Lighting in the yard, inside godowns and along the compound wall and provision of tower lights/watch towers. -Provisioning of handling equipments.

Q. 249.A 9 MT scrap material lot was sold at the rate of ` 25,300/- per MT in one of the stores depot in NCR in auction on dt. 10/10/2013. Calculate & reply following for the lot:

i) Total sale value

ii) Earnest money for the lot

iii) Balance sale value

iv) Last date for depositing balance sale value without interest.

v) Last date for free delivery.

vi) The purchaser wants to deposit the balance sale value in installments. How many installments (maximum) can be allowed in this case.

vii) The purchaser wants to deposit balance sale value on date 8/11/2013, then how much amount shall the purchaser deposit as interest (Base rate of SBI on the auction date was 10%).

viii) Purchaser took the delivery of the lot on date 5/12/2013. Calculate the amount of ground rent payable.

viii) Purchaser took the delivery of the lot on date 5/12/2013. Calculate the amount of ground rent payable.

Ans. i) Total Sale value = 253000 x 9 = ` 2, 27,700.00

ii) EMD = 10% of sale value = ` 22,770.00

iii) Balance Sale Value = ` 2,27,700 – 22,770 = ` 2,04,930.

iv) LDP = 20 days including auction day : 29.10.2013.

v) FDP = 50 days including auction day : 28.11.2013.

vi) Only 1 installment.

vii) Rate of interest will be = 17% (7% above the base rate of SBI) & interest shall be applicable for 10 days.

204930 x 10 x17 Interest amount = -------------------- = ` 967.72 = ` 968.

100 x 360 (Taking 12 months of 30 days each in a year) Else, if 365 days are taken in a year then interest amount will be 204930 x 10 x 17 -------------------- = ` 954.46 = ` 955.

100 x 365 Practically, it is calculated taking 360 days in a year. Hence if any candidate calculates it with 360 days (or 365 days) in a year it is to be treated as correct.

viii) Ground Rent: ½ % per day & Delay is of 7 days. (227700 x 7 x 0.5) GR = ---------------------- = ` 7969.5 = ` 7970. 100

204930 x 10 x17 Interest amount = -------------------- = ` 967.72 = ` 968.

100 x 360 (Taking 12 months of 30 days each in a year) Else, if 365 days are taken in a year then interest amount will be 204930 x 10 x 17 -------------------- = ` 954.46 = ` 955.

100 x 365 Practically, it is calculated taking 360 days in a year. Hence if any candidate calculates it with 360 days (or 365 days) in a year it is to be treated as correct.

viii) Ground Rent: ½ % per day & Delay is of 7 days. (227700 x 7 x 0.5) GR = ---------------------- = ` 7969.5 = ` 7970. 100

Q.250. Explain in detail the purchase order numbering scheme followed in N. C. Railway.

Ans. Purchase order numbering scheme:-

1) The purchase order number will be of 17 digits as shown below:- XX XX XXXX X XXXXX XXX Case No. Type of PO five digit PO No. PO item serial No.

1.1 First eight digits of P.O. No. represents the case number.

1.2 Type of order: XX XX XXXX X XXXXX XXX The 9th digit of the purchase order number signifies whether the order is a local purchase order or a rate/running contract order or Indent purchase or Boards contract. The relevant code nos to be allotted for different types of orders as well as their significance are indicated below. Types of order & their significance Code No.

a. Purchase order placed by COS on Foreign Suppliers. 0

b. Purchase order placed by the COS/Depot officers/Divl. Controller 1 of stores (Other than DGS&Ds rate & Running Contract orders).

c. Supply orders placed by the COS/Depot officers/Divl. 2 Controller of stores against DGS&Ds rate contract.

d. Supply orders placed by the COS/Depot officers/Divl. Corntroller 3 of stores against DGS&Ds running contracts.

e. Fabrication orders placed by the COS/Depot officers/Divl. Corntroller 4 of stores.

f. Indent placed on DGS&D and its Regional Directorates 6

g. Acceptance of tenders issued by the Rly. Bd.7

h. Indent/supply orders placed on production units 8

i. Indent/supply orders placed on the other Railways excluding Production units.

9 The appropriate code number as above should be incorporated for the 9th digit in the purchase order number.

1.3.1 Five digit P.O. Number:- XX XX XXXX X XXXXX XXX The Next 5 Digits i.e. 10th to 14th Digit Represent the Serial Numbers of the purchase order.

1.3.2 For orders placed by the COS Office, (one section will allot the serial nos centrally) the series listed below will be adopted for different categories of orders/Indent’s.

1.3.1 Five digit P.O. Number:- XX XX XXXX X XXXXX XXX The Next 5 Digits i.e. 10th to 14th Digit Represent the Serial Numbers of the purchase order.

1.3.2 For orders placed by the COS Office, (one section will allot the serial nos centrally) the series listed below will be adopted for different categories of orders/Indent’s.

ORDER SERIAL BLOCK

Stock Items Non stock items From To From To

Stock Items Non stock items From To From To

i) Indents 00001 00999 40000 40999

ii) COS Purchase orders 01000 34999 41000 45999 where payment is to be made by FA&COS

iii) DGS&Ds A/T Rate & 35000 36999 46000 47999 Running contracts & Rly Bds Orders

iv) Direct Delivery orders: (i.e. for non stock items delivered direct to the consignee). The serial block will be 60000 to 89499 and depending upon the paying authorities serial block as under will be adopted.

PAYING AUTHORITY FROM TO

iv) Direct Delivery orders: (i.e. for non stock items delivered direct to the consignee). The serial block will be 60000 to 89499 and depending upon the paying authorities serial block as under will be adopted.

PAYING AUTHORITY FROM TO

1. WAO/JHS 60000 62999

2. WAO/GWL 63000 65999

2. WAO/GWL 63000 65999

3. FA7CAO/C 690000 71999

4. SAO/C/JHS 72000 74999

5. SAO/C/AGC 75000 77999

6. SR. DFM/ALD 78000 80999

7. SR. DFM/JHS 81000 83999

8. SR. DFM/AGC 84000 86999

9. SAO (CSP)/SFG/ALD 87000 88999

10. FA&CAO/RPMU 89000 89499

1.3.3 Common 5 digit order serial number block for Depots/Divisional Material Managers are given below as under:- Stock items 50000 to 54999 Non-stock items 55000 to 59999

1.4 LAST THREE DIGIT OF PURCHASE ORDER XX XX XXXX X XXXXX XXXX The last 3 digits of the purchase order are a product of

(i) number of demands covered

(ii) No. of items included in the order

(iii) number of consignee. In case of severable contract the product is to be multiplied further by the number of delivery installments.

Q 251. What are the pre checks to be done by depot before issue of material on requisition submitted by indenting party?

Ans. Before issue of materials on requisition, the same should be checked to see that :-

a) the requisition form is filled correctly and there is no alteration or overwriting.

b) the requisition is signed by the authority competent to do so.

c) the certificate of fund availability is given.

d) the head of Account to which chargeable is given.

e) number of copies required are forth coming

f) one form of requisition contain only one item.

Q.252. In how many copies requisition-cum-issue note is prepared by indenter? What is the distribution and disposal of all the copies of requisition-cum-issue note ?

Ans. The "Requisition and Issue Note" should be prepared in six foils by the indenter in form no. S-1313. The indenter retains the first foil as his office copy. The other five foils are sent by him to the depot office which passes it on to the ward. After filling in the issue note portion by carbon process on all the five foils the ward keeper should distribute them as laid down below.

(a) The Second and Third foils:

These should be handed over to the Despatch Section along with the material. The Despatch Section will pass them on to the stores van clerk, if the material is being sent by the stores van, or send them to the indentor by post along with the Railway Receipt for despatch of the material. The indentor should retain the second foil and return the third foil through the stores van clerk or by the post as an acknowledgement for the material. This foil should be pasted to the depot's office copy of the issue note (the sixth foil). Any delay in returning this acknowledgement foil of the issue note should be promptly taken up by the Requisition Register Sub-section where the office copy foil (the sixth foil) should be inspected periodically in order to take up such omissions. The indentor should note on his office copy (the first foil) particulars of the Issue Note No., date quantity actually issued by the depot and latter forward the second foil to the District or Divisional Officer for check with the fifth foil which will accompany the summary of issues sent by the Stores Accounts Office of the District, or Divisional Officer.

(b) The fourth, fifth and sixth foils:

These should be forwarded by the ward-keeper to the Ledger Section along with the forwarding memo of issue notes. The sixth foil should be despatched by the Ledger Section and handed over to the Requisition Register clerks for posting the column "action taken" in the Requisition Register and for filling as record later on. The other two foils, (that is, the fourth and fifth) will be sent to the Stores Accounts Office (after the numerical ledgers have been posted) where one copy (the fourth foil) will be used for posting the priced ledgers .Org and later retained as record and the other (the fifth) will be used for preparing a summary of issues along with which it will be sent to the departmental officer for posting thereform the debits in his Revenue Abstract or other book of accounts. This copy will be retained by the departmental officer.

These should be forwarded by the ward-keeper to the Ledger Section along with the forwarding memo of issue notes. The sixth foil should be despatched by the Ledger Section and handed over to the Requisition Register clerks for posting the column "action taken" in the Requisition Register and for filling as record later on. The other two foils, (that is, the fourth and fifth) will be sent to the Stores Accounts Office (after the numerical ledgers have been posted) where one copy (the fourth foil) will be used for posting the priced ledgers .Org and later retained as record and the other (the fifth) will be used for preparing a summary of issues along with which it will be sent to the departmental officer for posting thereform the debits in his Revenue Abstract or other book of accounts. This copy will be retained by the departmental officer.

Q.253. Write short note on the following :-

a) Gate Pass

a) Gate Pass

b) Dispatch Section and procedure for dispatch of stores

c) Pending demand & disposal

c) Pending demand & disposal

Ans. a) Gate Passes.: No material may be allowed to go outside the gates unless specified on a Gate Pass or Authority for Removal of Wagons. Gate passes should be prepared in duplicate. Each Gate Pass (S. 1350) should show the following particulars.

(1) The number of men, with their ticket numbers.

(2) The number of packages.

(3) The number and date of voucher on which the material is sent.

(4) To whom sent and purpose for which sent.

(5) Whether Railway or Private Property. All material, except material loaded in lorries passing out of stores premises, should be examined and checked with the Gate Pass by the Gate Keeper, with the Assistance of the Chowkidars. For material loaded in lorries, a percentage only need checked. The Gate-keeper will also be responsible for seeing that all Gate Passes are correctly made out and that for the materials entered thereon, reference to an issue note or indent or some other letter or voucher is quoted. Gate Passes for material loaded in a lorry should show the number of packages in the lorry, and the total number of vouchers. All Gate passes should be scored across in order to prevent their misuse and then filed by the Gatekeeper in separate files for each section issuing them.

3.b) The work of despatching stores is an important function in the matter of the issue of stores and is best centralized in a Despatch Section independent of the wards and of the Ledger Section. This section may be divided into sub-sections, certain groups of stores being allotted to each for despatch. The men in this section should be properly trained in the know- ledge of stores in order to avoid mistakes in despatch. The Supervisor of the Despatch Section should also be in charge of the store delivery vans and the staff required for working them. The Despatch Section should maintain a Register of Despatches in Form S. 1345 to record all the issue notes handed over to the section for despatch of the stores. This register should show the following particulars :

1. Date.

2. Issue note number and date.

3. Consignee.

4. Requisition number and date.

5. Description of material and price list number.

6. Packing particulars- Quantity, Packing serial number, Packed in box, package, bag or bundle, Net weight, Gross weight.

7. Credit Note No. and date

.8. Railway Receipt No. and date.

9. Gate Pass or Authority to Remove Wagons, number and date.

10. Remarks (wagon number, &

C). This register should also serve as the Outward Wagon Register. The supervisor of the Despatch Section should present this register daily to the ward- keeper of each ward. The latter should personally fill in columns 1,2, 3, 4 and 5 with reference to all depot transfer forms and issue notes that are handed over to the Despatch Section. The Despatch Section should fill in the remaining columns of the register, columns 6, 7 and 8 not being filled in when material is despatched by store van, in which case only the number of the van need be entered in the remarks column.The Despatch Section will prepare the Credit Notes and make all necessary arrangements for the despatch of the material. 3

c) Pending demands are requisitions for supplies which have been received by a depot from indentors on the line, but which the depot has failed to satisfy due to the depot stocks of the stores asked for having been exhausted. When a ward is not able to supply a requisition either in part or in full and can offer no acceptable substitutes, the ward should attach to the requisition a printed slip carrying the legend 'NO STOCK' or 'Part Supply Made'. The requisition should then be sent to the Ledger Section. On receipt in the Ledger Section they should be entered in a 'Pending Demand Sheet' in form no. S-1336. The Pending Demand Sheets and the requisition forms should be retained in the Ledger Section until a fresh supply of material is received. In cases of part supply on combined "Requisition and Issue Note" Forms (S. 1313), the Ledger Poster should prepare a new set of forms to cover the balance of material not supplied. When the stock of any item is entirely exhausted, the ledger poster should attach a red slip to the ledger card to indicate this fact. When fresh material is received and this is being posted, the ledger poster should remove the red slip. Whenever he does this, he should see whether there is a pending Demand Sheet (S. 1336) for the item, in which case, the usual procedure of transmission of the requisition to the ward should be followed. The Depot Officer should send to the Controller of Stores once a fortnight a statement of pending requisitions in the form S-1338 to enable him to take prompt steps to remedy defects in recoupment of stores.

Q.254. Describe the procedure of receipt of workshop manufactured item in the depot .

Ans. In case of items manufactured in the Railway Workshops, the maximum and the minimum stock should be fixed taking into consideration the length of time required by the workshops to deal with the requisitions by Stores Depot and manufacturing process. Upon the Depot’s stock on an item dropping to the level of minimum, a requisition in Form S-1437, should be prepared in triplicate, first copy being in ledger section, second copy to Receipt Section and the third copy to Workshop’s Production Department. On receipt of requisition in the Workshop, the Production Engineer will plan for manufacture and issue a Work Order on a particular shop along with release order in prescribed form, for releasing raw materials, endorsing a copy to ledger Section and the Ward. After the receipt of raw materials from Stores depot attached to the Workshop, the Foreman of the Shop will take the manufacture process in hand. Upon completion of the order, the workshop will prepare a “Material Supplied to Stores” in Form S-1531 in five copies and distribute as under:

1 st copy - Office record of ward 2nd & 3rd - For Stores Accounts Officer through Ledger Section 4th copy - For Workshop Accounts Officer through Progress Office. 5 th Copy - Retained by Foreman as office record. The Receipt Section of the Stores Depot having duly checked the items of stores received, should endorse receipt on all the five foils and return the 4th copy to Production Department. The remaining three copies, duly receipted should be sent to the ward along with materials. The ward should allot R.O. number to them and forward them along with the forwarding memo(S-1256) to Ledger Section where the quantity received should be posted. One copy should be forwarded to Stores Accounts Officer who will submit 2nd foil to the Workshop Accounts Officer in support of the Advice of Credit(S-2705) to stop, retaining the third foil as record.

Q.255. What do you understand by Forecast Schedule of Stores prepared by workshop? Describe the procedure of issue of material to workshop?

Ans. Forecast schedules of all stores, tools, assemblies and fittings and component parts required by the workshop for periodical overhauls of rolling stock should be prepared as early as possible in advance of the actual day on which they would be required and these schedules should be furnished to the subward-keeper to enable latter to keep such materials ready for early issue. These schedules should be submitted over the signature of the Works Manager or a gazetted officer working under him. Such forecasts should not be issued piecemeal, one consolidated forecast should be made out for the rolling stock expected to be overhauled in the month. All materials required by the shops shall be drawn, only as and when required, the requisitions being made in carbon duplicate on "issue tickets". The sub-wardkeeper should obtain the signature of the employee receiving the stores on both the foils of the issue ticket in respect of the stores supplied to the latter. The duplicate foil should be returned along with the material to the receiving chargeman. Early every morning, each shop office should arrange the chargeman's copies of the issue tickets of the previous day (which give particulars of the materials received that day) in the order of 'class and price list numbers. The issue tickets bearing the same price list number should than be re-arranged, work order by work order, and a pencil abstract made on the back of the last issue ticket for the day of each item of stores issued, of the total quantity of that item for each work order. Combined 'Requisition and Issue Notes in form S-1523, should then be prepared in carbon quadruplicate, all items of one group supplied during the day being entered in one workshop Issue Note. Separate Workshop issue note should be prepared in respect of materials obtained from the parent ward as distinct from the sub-wards. The sub-ward-keeper (or ward-keeper in the case of an issue from the parent ward) will retain one foil of the workshop issue note as his record and send two copies along with necessary forwarding memo (S-1256) to the Ledger Section of the depot for the posting of the numerical ledgers. They should later on be passed on to the Stores Accounts Officer who after pricing the issue note and posting his priced ledgers will send one foil, with a Daily Summary of Issues (S-2702) to the Workshop Accounts Officer. The Workshop issue note should be checked by the ward keeper with his copies of issue tickets. The sub-ward keeper should retain three copies and return 4th and 5th copies to indenting foreman. The sub-ward-keeper should hand over his record copies of the Workshop-issue notes to the main ward-keeper in order to recoup himself. The foreman will daily submit one copy of the issue notes received by him to the Works Manager or a Senior Subordinate specially empowered by the Chief Mechanical Engineer, who should scrutinize the issue notes, as they indicate the nature and the scale of the daily consumption of materials, sign them in token of having accepted them and forward them to the Workshop Accounts Officer, daily. The other copy will be retained by the foreman as his record. The shop foreman will be responsible for seeing that the workshop issue notes for the day are obtained from the Stores Department and submitted to the Works Manager before noon of the day following.

Q.256. What are the categories of stores returned by workshop? How they are accounted in the depot and show the disposal of copies of returned stores of workshop?

Ans. Stores Returned by Workshops: Returned Stores may consist of.

(1) Surplus Stores being balance of new materials that have not been used on a work

(2) Stores released from works;

(3) Tools and plant no longer required; and

(4) Scrap. All such material should be handed over promptly, on the authority of an Returned Stores (S-1579) to the sub-ward-keeper of the shop, whose duty it shall be to see that the materials are valued by the Stores Department, despatched to the account therein. There is no objection to the sub-ward-keeper avoiding a physical transfer of such of the material as it is possible for him to set off against the issues of the day. He is prohibited from accumulating any stores or scrap that are not required in the shop to which his sub-stores is attached. The Advice Note of Returned Stores should be prepared in five foils. Separate Advice Note should be prepared for each group and for new, secondhand, scrap and condemmed materials and should show the nomenclature and other particulars of the stores, the head or heads of account to be credited as well as the rates and value of the stores. Separate serial numbers should be given for Advice Notes originating from each shop. The foreman returning to stores should retain one copy as his block foil and send the remaining four foils alongwith the materials to sub-ward-keeper. The materials should be checked with the Advice Notes and arranged for inspection and valuation by the Depot Officer or a gazetted officer on his behalf. Immediately after the stores are valued, the sub-ward-keeper should complete the four foils in this respect, take the stores into stock (either his own or that of the parent ward) and initial the advice Notes and send them to the depot office through the parent ward where they should be assigned R. O. numbers as usual. The four foil, after signature by the Depot Officer or a gazetted officer on his behalf, should be disposed of, as follows : The first foil retained as record, The second foil sent to the returning officer, The third and fourth foils sent to the Stores Accounts Office after the numerical ledgers have been posted. The Stores Accounts Office after posting the priced ledger should prepare a summary of credits to the shops, for stores returned to the depot each day. The third foil of the Advice Note alongwith a summary of credits (S. 2705) will be sent by the Stores Accounts Officer to the Workshop Accounts Officer to post the Registers of work orders or Allocation Registers for revenue abstracts. The fourth foils of Advice Notes (S-1539) will be filed in the store Accounts Office. The second foil of the Advice Note should be submitted to the Workshop Accounts Office through the Works Manager, who will scrutinise them before countersignature to see that the credits are afforded at reasonable rates by the Stores Department. This scrutiny may be carried out by a selected subordinate specially empowered to do so by the Chief Mechanical Engineer. The Workshop Accounts Office should arrange the second foils of the Advice Notes (S-1539) by shops and the order of the numbers and dates given by the shops and should pair such foils with the third foils received from the stores accounts Office along with the Advices of credits (S-2705) Any cases of delay in affording credits or discrepancies in quantities etc., should be taken up each fortnight for the Advice Notes of the previous fortnight with the Depot Officer.

Q.257. What is the procedure of receipt and issue of serviceable items from Stores?

Ans. Advice notes for material which though unserviceable, could after reconditioning or repairs be rendered serviceable and would thus be useful for another term of life, should be accepted as "Repairable." Credit should be afforded by the Stores Depot for wholly and partly ferrous articles at 1/3rd and non-ferrous articles at 1/2 of the current book rate for the new articles. Such articles would generally be stock items of locomotive, carriage and wagon parts and fittings. Separate ledger cards under their relevant price list number affixing the correct category code to the price list number of the new article, should be maintained for repairable ones. As soon as it is desired or advantageous to do so, the Stores Depot should get the repairable material made serviceable for issue to consuming department for adding to serviceable stock instead of ordering for new materials. The repaired articles should be taken on books at the book rate for repairable ones plus the actual cost of repairs or average cost of repairs, as convenient. No distinction should be made between new and repaired articles in the matter of storage, and the issue prices of the materials should be the same.

Q.258. Explain briefly the preservation technique of the following.

a) Rubber items

b)Timber and Wooden items

c) Chemical Acids

d) Batteries

e) Electrode

f) Paints

g) Explosives Fog Signal

Ans. a) Rubber Items:

Rubber stores should be stored in very cool room. Stores should be frequently dusted with adequate French chalk. Rubber stores should be kept away from heat such as Electric Motors, Generators and also away from oil, grease and acids.

b) Timber and Wooden Items:

Timber should be protected from micro-organisms as to avoid moist timber which results damage, change of coloour and loss of strength and weight. It should also be protected from getting Wet, either from rain water or leaks or moistures from ground. For protection from insect borer, shall be treated with insecticides prescribed and also painted or varnished and be treated with fungicides.

c) Chemical Acids:

Various types of chemicals should not be mixed up. Stoppers should be kept plastered to prevent from moisture. Containers shall be kept on level floor in sand cushioning in cool and well ventilated sheds.

d) Batteries:

They should be kept in cool and dry racks and terminals protected with a coating of grease. Dry cells should be stored in their original cartons. Old batteries should be issued first. If due to some reasons the acid cells are kept in storage for a long time, the acid solution should be replaced.

e) Electrodes:

The flux coating of the electrodes is likely to get off the metal rod either by absorption or moisture or by mechanical rubbing. They should be stored in original moisture proof cartons. Mechanical rubbing should be prevented during handing.

f) Paints:

Paint drums should be turned upside down or rotted first after 3 months of the storage, and then after every 15 days. Retail issue should be avoided and if made the drum should be soldered back at once. First in first out principle should be observed for issue. Paints should be stored in cool place.

g) Cement:

Cement gunny bags should be stored in leak proof sheds and floor should be pucca or suitable dunnage should be used. A clearance of at least one foot from the walls and roof should be left. Gangway of 3 feet should be left for handling. Chances of outside rain water coming inside should be avoided. Oldest receipt should be issued first.

h) Leather goods:

Leather goods be sorted in cool well ventilated shed. Care should be taken to dust regularly and old stock should be issued first.

Q.259. What do you mean by imprest stores? How is imprest recouped? Show the disposal of foils of imprest schedule.

Ans. Materials whether stock items or non-stock items, held in stock at Running Sheds, Train Examining Stations etc., not for specific works but as a standing advance for the put pose of meeting day to day requirements in connection with the repair and maintenance and operation of rolling stock shall, including consumable stores such as cotton waste, jute, oil, grease, etc., be treated as imprest stores, so long as they are under the control of the authority in charge of the executive unit, and have not been issued to works. The material required to upkeep of rolling-stock, by divisional electricians and that required for house lighting purposes at various stations by electric chargeman should also be treated as imprest stores. Each imprest holder should close his ledgers monthly on the dates fixed for him and check them with the issue and recoupment schedule prepared in form S-1830 from the monthly summary of issues in four copies, out of which three copies should be sent to the Stores depot which is assigned as Supply Depot. The imprest holder shall ordinarily recoup the full quantity necessary to bring up his balance to the fixed imprest. The quantities demanded in recoupment of imprest should be the total issues minus such receipts, i.e., the quantity required to bring up the stock to the sanctioned level. The Depot Officer should enter in the copies of the Recoupment Schedule (S. 1830) the quantities of materials actually issued against the quantity demanded. If the former is different from the latter, the balance of the indent is automatically cancelled. The imprest holder may recoup the balance through the next schedule or through a special recoupment schedule as and when necessary. Two copies of the issue and recoupment schedule as completed by the Stores Depot should be sent along with the material Acknowledgements for the material supply should be obtained on both the copies from the imprest holder. One copy will be held by the depot as receipt, while the other copy will be submitted by the imprest holder to his District or Divisional office for check with the copy received from the Stores Accounts Office. The remaining two copies of the schedule be sent to the Stores Office after the depot, numerical ledgers have been posted from one of the copies. The Stores Accounts Office should insert the rates on the schedules, and after valuing the actual quantities issue by the depot separately for each head of account, should post the relevant priced ledgers, and forward one copy to the Divisional or District Officer concerned in support of the Daily Summary of Issues (S. 2702). The other copy will be retained for record in the Stores Accounts Office.

Q.260. Identify the end use of following materials in railways.

a) Pantograph

b) Suspension bearing

c) Fiber reinforced lubricating pads

d) PVC Flooring

e) Center Pivot Guide

f) Lube Oil Filter

g) FREON Gas 22

h) Carbon Brush

Ans. a) Pantograph: Pantograph is an important component of the EMUs and Electric Locomotives. It has a copper plate on its top which touches the overhead contact wire. Thus, it collects the current from contact wire and transmit it to EMU or electric locomotives.

b) Suspension Bearings: There are journal type of bearings and have white metal lining on its inside surface. These bearings are used in WDM2 locos and also on SDM2 types of electronic locomotives.

c) Fiber Reinforced Lubricating Pads: Fibre re-inforced lubricating pads are used in suspension bearings for lubrication between axle and bearings by wick principle.

d) Distribution Valves: Distribution valves are used in wagons and coaches which are working on air brake system, and in locomotives having twin brake system. This valve actuates the braking action whenever the pressure in brake pipe is destroyed it.

e) Freon Gas 22: This gas is used generally in the cooling system of airconditioners and coolers.

f) PVC Flooring: PVC Flooring consists of Poly Vinyl Chloride sheets or PVC sheets used in the flooring of toilets and lavatories of coaches, and hence formed as PVC flooring.

g) Centre Pivot Guide: Centre pivots of the chasis rest on the Centre pivot guides provided in bogies. These guides of locomotives transmit the load of the engine to the bogies.

h) Lube Oil Filter: The lube oil filter is used in the lubricating oil system of the diesel locomotives and filters the floating particles from the lubricating oil before it is supplied into the lubricating system of the engine.

i) Carbon Brush Tao-659: This carbon brush is lused in the TAO 659 type of traction motors fitted in AC Electric Locomotives. These carbon brushes transmit electricity to the commutator of the traction motors.

Q.261. What is depot transfer? How is SINT Suspense cleared ?

Ans. The transfer of stores from one depot to another is called depot transfer. When the stores issued during a month from a depot are not received in the receiving depot in the same month, such items would not appear in the accounts of the receiving depot. The issuing depot would submit summaries of issues to the receiving depot concerned and that the receiving depot should note down on the summaries the dates of accounted of each of the items as they are posted in the priced ledgers. At the same time a preformed summary of receipts is prepared for the month by the Accounts section .At the end of the month, unaccounted items in the issue summaries should be posted into a register styled "Register of Stores-in-Transit." maintained and their clearance should be watched carefully. When any such item is accouted for later, the credit should be posted in the register in the column for the month of accounted and against the debit entry for the item concerned. Separate registers should be maintained for each depot. The balances lying in the Stores -in Transit Registers should be carefully analysed each month and if any item has been found to be outstanding for more than one month, the matter should be taken up with the Depot Officer concerned. Special lists of items outstanding for more than three months should be sent to the Controller of Stores for taking steps for their clearance.

Q.262. Differentiate between the following.

a) SINT Depot and SINT Purchase

b) Imprest store and Custody store

Ans.. a) Stores-in-Transit 'Depot'. - When the stores issued during a month from a depot are not received in the receiving depot in the same month, such items would not appear in the accounts of the receiving depot. The issuing depot would submit summaries of issues to the receiving depot concerned and that the receiving depot should note down on the summaries the dates of accounted of each of the items as they are posted in the priced ledgers. At the same time a preformed summary of receipts is prepared for the month by the Accounts section .At the end of the month, unaccounted items in the issue summaries should be posted into a register styled "Register of Stores-in-Transit." maintained and their clearance should be watched carefully. When any such item is accounted for later, the credit should be posted in the register in the column for the month of accounted and against the debit entry for the item concerned. Stores-in-Transit 'Purchase'. - The credits to Purchases Account are posted from the Receipt Notes granted by the Stores Depot. In cases where Inspection and Receipt Work is centralized such receipts are granted on behalf of the Stores Department by the Receiving and Inspecting" Officer. The posting of such receipts in the priced ledgers as a contra debit entry will appear however only when the material has been received by the Depots stocking the items and accounted for by it in its priced ledgers. In such cases the Receipt Notes granted by the Receiving and Inspecting Officer towards the close of a month would appear as credits to Purchase Account whereas the complementary debits would not appear in the same month in the priced ledgers as the materials would not have reached the stocking depot within the month.

b) Imprest Stores: Materials whether stock items or non-stock items, held in stock at Running Sheds, Train Examining Stations etc., not for specific works but as a standing advance for the put pose of meeting day to day requirements in connection with the repair and maintenance and operation of rolling stock shall, including consumable stores such as cotton waste, jute, oil, grease, etc., be treated as imprest stores, so long as they are under the control of the authority in charge of the executive unit, and have not been issued to works. The material required to upkeep of rolling-stock, by divisional electricians and that required for house lighting purposes at various stations by electric chargeman should also be treated as imprest stores.

Custody Stores: These stores chiefly consist of items obtained for the Mechanical Department for the construction of rolling stock/sanctioned under the Capital or Revenue Programme. Directly the stores are received and paid for, the cost is at once debited to the works concerned. Instead of the stores lying in the workshops until they are required, the stores Department should keep them in safe custody, proper numerical records being maintained by the department.

Q.263. What do you understand by Departmental stock verification? Under what circumstances the Depot Officer can waive off departmental stock verification?

Ans. Department Stock Verification- As an important back check on the correct receipt and issue of stores by the Wards, it is necessary to have a departmental check to see whether the up-to-date balance of an item in the ledger agrees with the actual physical stock balance. Such departmental verification to be arranged by the depot officer will be in addition to the Stock Verification arranged by the Accounts Department. The departmental verification need only cover selected items such as items of large annual consumption having regular and frequent issues, items of heavy value like non-ferrous items, tool steel, etc., and items of a pilferable nature. A list of such selective items may be drawn up and approved by the Controller of Stores. The verification of physical balances should be done by an official other than the Ward-keeper-in-charge of the item of Stores. The depot officer may postpone the verification if the balances in stock are so heavy that a verification would involve large shifting of stock and the verification could be carried out conveniently at a later date when stocks are at a low level. The Depot Officer may waive verification in the following circumstances.

(a) Where the item has been verified by the Accounts Department within the last three months.

(b) Where the Accounts Verification of the particular class of stores is in progress and, the item is likely to be verified within the next two months.

(c) Where the item has heavy balances the verification of which involves much labour and handling charges.

Q.264. What do you mean by authority for removal of wagons? What is traffic statement of wagons and how it is dealt?

Ans. No wagons may be removed from the Yard unless the Traffic Department is in possession of the Authority for removal of wagons. Traffic Statement of Wagon- The traffic Department will submit weekly in duplicate statements of all wagons booked from or placed in the stores yard showing the wagon number, date of removal from or placing in the yard, consignor and consignee, net weight, and brief description of contents. Both copies will be sent to the Depot Store-keeper. On receipt of this statement, the Yard Foreman should compare it with his wagon registers (S. 1215 or S. 1345) and quote the corresponding issue note number and the weight of material shown thereon against the wagons that have gone out of the yard. Similarly, particulars should be shown for wagons received, the information should be tabulated on a slip to be pasted to the Traffic Statement. He should then put it up to the Depot Store-Keeper who should personally check 10 % of the entries with all connected vouchers. If the Yard Foreman notices any discrepancy, he should at once bring it to the notice of the Depot Officer. The statements should then be pasted in a Skelton file. The Depot Officer should check these statements once a month.

Q.265 Write short note on following.

a. Local Purchase

b. Lead time

c. Buffer Stock

c. Auction Catalogue

d. Direct Sale

Ans.

(a) Local Purchase - The Controller of Stores may make local purchase if items of small value, both stock and non-stock, up to Rs. 1,00,000/- per item- subject to fulfilment to conditions laid down in para 711-S.

i) The normal annual recoupment quantity does not exceed Rs.100000/- in value : or

ii) The stock of the item is precariously low and the same is urgently required, and that the quantity is not deliberately reduced with a view to brining the purchase within the scope of this provision.

(b) Lead Time - Lead Time is the time taken from the date of realization of need of recoupment (i.e. date of recoupment) to the physical receipt of material at the stocking place. Knowledge of Lead Time is very important for effective design of any Recoupment system. Lead Time often is not constant and therefore variations in Lead Time also play very important role.

(c) Buffer Stock- In spite of best calculations, there is a variation in lead-time and consumption pattern. To cater to the fluctuations of lead-time and / or consumption pattern, buffer stocks are required. In any recoupment system, we work out the quantities to be recouped on some forecasts of annual consumption and lead time. However, the actual figures may deviate from the forecast figure and this will lead to a situation of either stock out or overstock at some point of time. To avoid stock outs, we often provide safety stocks which are also known as buffer stock.

(d) Auction Catalogue- Before the auction is conducted; time, date, venue and the items to be included in the auction are put in a booklet for circulation to the prospective bidders. This booklet is called Auction Catalogue containing description, lot no., quantity, location of items to be sold through auction and detailed terms & condition governing the auction sale. The auction catalogue is printed for distribution to all concerned for wide publicity by the Stores Depot which indents to dispose off the scrap through auction. It is also uploaded on the website of the railways.

(e) Direct Sale- Direct sale is sale of railway stores without calling tenders. Direct sale is generally made to other government departments, other zonal railways or to railways contractors for use on the railways works. Some scrap items are disposed off by direct sale to railway employees for their bonafide use at approved prices with concurrence of accounts. The rates are generally based on last auction rates/book rates.

Q.266 (a). What are the various methods of despatch of materials from supplier to Stores Depot ?

(b). What is procedure for preferring claim with carrier when the material is received short at Stores Depot ?

Ans.

(a) Materials are dispatched by the suppliers to the Stores Depot:-

i. Through Railway Parcel or Full wagon loads or containers or lorries.

ii. Through Lorries and Carts from local suppliers.

iii. Through authorised representative of the Railways, in case of urgency.

iv. Through Post Office Parcel/Couriers

v. By Steamer/Ship or Air or through post-parcel in case of Imported Stores

Ans. (b) When the package is cleared from Goods shed/parcel office, Depot should demand for open delivery from the commercial department, if the package is damaged outwardly. After the open delivery has been granted, a joint survey report is made out by the commercial department with representatives of Security and Stores department, in case any shortages are revealed. The delivery of the consignment is taken, duly recording suitable remarks in the delivery book. Claim is preferred o Commercial department, enclosing a copy of joint survey report for the stores damaged/received short. If packages are not damaged outwardly and if there is no difference in weight, we cannot prefer claim on carriers. Even if it is not damaged, if there is difference in weight, it should be recorded in the delivery book and open delivery is demanded.

Q.267 (a). How are claim of shortage/Breakage/damage to be settled?

(b). What are major categories of scrap into which Railway Scrap classified?

Ans. (a)Consignments, against RR/PW Bills if not delivered within a reasonable time by the carriers, are required to be claimed within six months from the date of booking / date of R.R. As the claims on carrier are to be preferred within six months, timely action is required to be taken so that the claims do not become time- barred. Therefore the RRs / PW Bill Registers are periodically reviewed by the Depot Officer. If during this review it is seen that a consignment has not been received within a reasonable time (45 to 90 days) a missing report is sent to all concerned with a copy to CCS. For such cases a manuscript register (Claims Register) with may be maintained. The claims should be preferred in time, i.e., within six months from the date of booking. Normally, claims will be accepted by the commercial department, based on the joint survey report, which is necessary for claiming for shortages, breakages, and damages. In case of its non-settlement within 6 months from the date of claim, it should be discussed between the claimant and the claims departments at officers’ level. In case a settlement is not arrived at even at this level, meetings should be arranged at higher levels, right upto HOD’s level by the claimant. If the settlement of the claim is not reached within one year, even at the HOD level, the case will be put-up to Additional General Manager through Chief Claim’s officer for final decision.

Ans. (b) Workshops, diesel, electrical, wagon depot sheds, engineering and signal workshops, engineering departments with PWIs/BRIs/IOWs, etc. and signal departments are the major centres for generation of Scrap Important categories of scraps are –

i. Industrial scrap

ii. Re-rollable scrap

iii. Melting scrap

iv. Cast Iron scrap

v. Condemned Rolling stock

vi. Bronze scrap

vii. copper scrap

viii. Other Non-ferrous scrap

ix. Scrap machinery

x. Piper and Pipe fittings

xi. Wooden scrap

xii. Waste paper

xiii. Condemned boiler

xiv. Steel cut pieces xv. Condemned furniture

xvi. Empty receptacles.

Q.268 How the cash imprest account for making local purchase is to be maintained and recouped? Ans. i A cash book is maintained by the concerned local purchase supervisor.

ii. All purchasers are made as per established rules and clear receipted cash vouchers are obtained from the suppliers for every purchase on stamped bill. These are allotted serial numbers and are entered in the cash book with serial numbers.

iii. When the cash on hand reaches a stage, which will cover the period that will be taken to recoup cash, recoupment voucher in the prescribed proforma in form No.712 is prepared in 4 copies and sent to the accounts officer, duly signed by the Depot officer, supported with the relevant cash vouchers.

iv. All the cash vouchers also should be attested by the Depot Officer, besides recording the acceptance on the relevant tender/quotation.

v. A. Certificate viz, “Certified that the above purchase, have been made in terms of para 711-S and the stores have been put into stock”. Is to be recorded by Depot Officer on each recoupment voucher.

Care should be taken to see only one group of stores is included n each recoupment voucher.

vi. After acceptance of materials, one copy should be retained as office copy, one sent to Accounts Officer/Stores along with cash vouchers for recoupment of imprest cash, as specified in para(iii) above, one to Controller of Stores and the last to the Stores Accounts (through ledger, in the case of stock items only) for necessary action/record.

vii. Allocation particulars are shown in each voucher.

viii. These vouchers are scrutinized by respective Accounts Officers and they are passed for payment, duly sending a Cheque to the Chief Cashier who arranges payment. Depot Officer collects cash, if he is not having cheque facility. ix. In the case of system of operating with cheque and Bank account, the cheque is sent to the Bank direct, for crediting the account of imprest holder. Thus, the cash is recouped by the Depot Officer.

Q.269. “Knuckle Thrower” is a RDSO approved item used in wagon maintenance in the workshop. The item is urgently required in General Stores Depot in N.C.Railway consisting officers of 1 Dy. CMM, 1 SMM and 2 AMMs. The stock, AAC & dues position as on 10.10.2013 is given below : Stock = 0 AAC = 1500 Nos Covered Dues:- 1500 Nos. PO No.1234 date 01.10.2013 placed by COS office On M/s XYZ DP 31.03.2014 with Basic rate @ 305/-,ED@ 12.36%extra, CST @ 5% extra Freight@Rs.10/- Inclusive. (Firm M/s XYZ has informed that it will dispatch the material after 01.02.2014) The local purchase sheet was initiated by the Léger keeper for 375 nos with value of Rs.137812/- based on last successful purchase rate @ 350/- +CST @ 5% extra. Against PO No.6789 dated 01.01.13 to M/s ABC,DP-31.03.13 (PO completed). The local purchase tender was opened on 15.10.2013 and lowest offer was received from M/s ABC @ Rs.325 + CST @ 5% extra, ED@ 12.36% (Inclusive), Freight Charges @ Rs 15/- each extra, Inspection –consignee, DP within 21 days from date of receipt of PO. The firm M/s ABC is RDSO Part-I Approved firm and has quoted the description as per tendered description without deviation. In view of above situation, explain the following.

(a) State whether the local purchase sheet initiated by ledger keeper was justified or not?

(b) State whether the local purchase PO could be placed on lowest offer firm M/s ABC or Not.

(c) Who would be competent authority to decide this local purchase case and obtain the total purchase order value if PO placed for full tender quantity?

(d) What would be delivery period date on PO, if PO was placed on 17.10.13 and despatched on same date to firm?

Ans. (a) The material is Out of Stock in the depot and urgently required. Although the PO No. 1234 dated 01.10.13 has been placed on firm M/s XYZ with DP30.03.14., M/s XYZ has informed that it will supply the material after 01.02.14. In case of urgently required stock Item, the depot officer has been given powers upto Rs 3 Lakhs per case. As M/s XYZ will despatch the material after 01.02.14, the quantity of 3 months requirements should be procured within depot officer’s power for this period. The AAC of this item is 1500 Nos. Hence, 3 month requirements would be 375 Nos.. Hence, the Local Purchase Sheet placed by the ledgerkeeper for 375 nos for Knuckle Thrower was justified to meet out the urgent requirements of the workshop.

(b) The lowest offer has been received in the tender opened on 15.10.13 from the firm M/s ABC@ Rs.325 + CST@ 5% extra, ED@ 12.36% (Inclusive), Freight Charges @ Rs 15/- each extra, Inspection –consignee, DP within 21 days from date of receipt of PO.

(i)The firm M/s ABC is RDSO Part-I Approved firm and has quoted the description as per tendered description without deviation. Hence, the offer of M/s ABC if found technically suitable.

(ii)The firm M/s ABC is also last successful supplier against PO No. 6789 dated 01.01.13. In view of above (i) and (ii), the offer of M/s ABC can be considered for placement of full quantity based on technically suitability and past performance. The all inclusive rate against PO No. 1234 dated 01.10.13 placed by COS office would be Rs. 359.83 /- each. The all inclusive rate against completed PO No. 6789 dated 01.01.13 would be Rs. 367.50 /- each. The firm M/s ABC has quoted all inclusive rate of Rs. 356.25 /- each which is lower than the all inclusive rate of PO No. 1234 dated 01.10.13. as well as the all inclusive rate of PO No. 6789 dated 01.01.13. Hence, the rates quoted by the firm M/s ABC in this tender is found reasonable. As the offer of M/s ABC is found technically suitable and rate is found reasonable, the local purchase PO can be placed against lowest offer of M/s ABC.

(c) The tendered quantity is 375 nos. The lowest offer has been received in the tender opened on 15.10.13 from the firm M/s ABC@ Rs.325 + CST@ 5% extra, ED@ 12.36% (Inclusive), Freight Charges @ Rs 15/- each extra. All inclusive rate of this offer would be worked out@ Rs 356.25 /- each. Hence, Total Value of PO= Rs 356.25 x 375 = Rs. 133593.75 SMM in the depot other than independent charge has been given power upto Rs 1.50 lakhs per case. Hence, SMM will be the competent authority to decide this local purchase case. The total purchase order value will be Rs. 133593.75 .

(d) The firm M/s ABC has offered DP as 21 days from the date of receipt of PO. There would be 1 week (7 days) transit time to receipt the PO by firm from the date of despatch. Total 28 days delivery time should be given in PO. If the PO has been placed on 17.10.13 and has been despatched on same date, the Delivery Period date on PO will be 13.11.2013.

Q.270 Details of an Public Auction Sale in the E-Auction of a depot relating to ferrous scrap are given below : Date of E-Auction : 20.09.2013 Qty. Sold : 250 MT Rate accepted : Rs.24000/-PMT Calculate the following discussing in detail as per the relevant rules and condition.

(a) The amount of EMD to be deposited on auction date in E-Auction.

(b) The BSV and the last date of payment for Balance Sale Value without interest including number of installment permitted.

(c) What will be last date of payment with interest charge if the firm failed to depots BSV within free time of payment ?

(d) Interest payable for delayed payment if firm deposit BSV on 20.10.2013 (Base rate of SBI as on 20.09.2013 was 9%)

(e) Calculate the Free Delivery Time and max. Extended Delivery Period with Ground Rent within Dy. CMM /Depot power .

Ans. Date of E-Auction : 20.09.2013 Qty.

Sold : 250 MT

Rate accepted : Rs. 24000/-

PMT Total Sale Value = 24000 x 250

= Rs. 60,00,000 /- (Rs 60 Lakhs)

(a) As per the current sale of condition in E-Auction, 10% of the sale value will be deposited as Earnest Money for the sale of lot .

Total Sale Value = Rs 60,00,000 /- Hence, EMD

= 10 % of Rs 60,00,000 /-

= Rs. 6,00,000 /-

(b) Balance Sale Value (BSV) = Total Sale Value – EMD

= 60,00,000 – 6,00,000

= Rs. 54,00,000 /-

Balance Sale Value (BSV) for the lot valued above Rs 1 Lakh should be deposited within 20 days from the date of auction (including Auction Date) and 3 installments for lots valued above Rs 10 Lakhs may be permitted.

In this case, Last Date of Payment for depositing BSV without interest charges (Free Time of Payment) will be 09.10.2013 and max. 3 installments may be permitted for this.

(c) If the firm failed to deposit BSV within free time of payment, the last date of payment can be extended by the Railway Administration at the request of the purchaser subject to levy of Interest Charges for the Belated Period (not beyond 40 days) including the date of auction.

Hence, the last date of payment for BSV with interest charges would be 29.10.2013

(d) Base Rate of SBI as on 20.09.13 was 9 %. Interest Rate in case of delayed payment will be charged @ 7% above the Base rate of State Bank of India applicable as on date of auction.

Free Time of Payment would be upto 09.10.13

The last date of payment for BSV with interest charges would be 29.10.2013. The firm has deposited the BSV of Rs. 54,00,000 on 20.10.13.

The interest charges will be calculated on Rs. 54,00,000/- with interest rate@ 16% for belated 11 days.

Hence, Interest Charges payable = 54,00,000 x (16 /100) x (11 / 365)

= Rs. 26038.3

= Rs 26038 /- (round off)

(e) The Free Delivery Period (FDP) allowed for the sold lots is 50 days including auction date. Hence, FDP in this case would be 08.11.2013. Dy. CMM/ Depot can extend the Delivery Period with Ground Rent for delivery of Scrap upto 65 days from the auction date.

Hence, Max. Extended Delivery Period Date with Ground Rent within Dy. CMM/Depot power would be 23.11.2013.

Q.271. The item ‘X’ is safety and category- C item and used in POH of wagons. The detail as given bellow.

CP : 01.04.2014 to 31.03.2015

AAC for 2013-14 :1800 Numbers (based on POH outturn target for 2013-14).

POH outturn target for wagons in year 2013-14 = 75

wagon per month POH outturn planned for wagons from year 2014-15(from 01.04.2014) = 100 wagon per month .

Stock in hand on 01.10.2013 = 200 Nos Covered dues = 300 Nos.

Calculate the following ?

(a) The AAC Qty. requirement for year 2014-15

(b) The Net IP requirements

(c) The CP requirements

(d) Net requirement upto 31.03.2015

Ans. (a) AAC for 2013-14 =1800 Numbers (based on POH outturn target for Year 2013- 14).

POH outturn target for wagons in year 2013-14 = 75

wagon per month Hence, POH outturn target for complete year 13-14 = 75x12 = 900 wagons.

Hence, Qty. of items used in 1 wagon = POH outturn per year / AAC = 1800 / 900 = 2 nos.

POH outturn planned for wagons from year 2014-15(from 01.04.2014) = 100 wagon per month .

Hence, POH outturn planned for complete year 2014-15= 100x12 = 1200 wagons.

Hence, Qty required for 1200 wagons in 2014-15 =1200 x 2= 2400 Nos.

Hence, AAC quantity requirement for year 2014-15 will be 2400 Nos.

(b) Contract Period : 01.04.14 to 31.03.15 Stock in hand on 01.10.2013 = 200 Nos Covered dues

= 300 Nos. Interim Period will be from 01.10.13 to 31.03.14 for 6 months.

AAC for period 01.04.13 to 31.03.14 = 1800 nos. MUF for 2013-14 = 1800/12 =150 nos This is a Safety and Cat- C item, so Buffer Stock of 3 months is being taken. Net IP requirements upto 31.03.14 = 6 month requirement + Buffer Stock – (Stock +Dues) = (150 x 6) + (150 x 3) – (200 + 300) =850 Nos. (c) The POH outturn Ennhanced for wagons from year 2014-15(from 01.04.2014) = 100 wagon per month = 1200 Wagons per year Hence, AAC for year 2014-15 = 1200 wagon per year x 2 nos per wagon = 2400 Nos. Hence CP requirements for 2014-15 = 2400 Nos. (d) Net Requirements upto 31.03.15 = Net IP requirements + CP requirements = 850 + 2400 = 3250 Nos

Q.272. (a) What are the necessary requirements for registration of bidder for participating in E-auction with IREPS application?

(b) How can a bidder register itself ONLINE with IREPS application for participating in E-Auction?

Ans. (a) Registration with IREPS site (www.ireps.gov.in) is must for any bidder to participate in E-Auction for Indian Railways. For registration, bidder needs to have valid Class III Digital Signature Certificate with Bidder’s Firm Name issued by licensed Certifying Authorities, an affidavit duly notarized on stamp paper of requisite value and valid Email ID and one time Registration fee Rs. 10,000 . They also need to have a computer with Internet browser (IE 6 or IE 7) and Internet connectivity. Without valid Digital Signature Certificate and User ID, vendor cannot participate in E-Auction. The bidder can either go for Online Registration or Manual registration by Railway user in Depot.

Ans. (b) Bidder must open "New Bidder " link ( at top left page of www.ireps.gov.in) from Auction Home page and fill login registration form. After submission of filled up form, bidder will be directed to Payment Interface for Payment of Refundable registration fees of Rs. 10,000 through Payment Gateway/ Net Banking facility of various banks. After submission of registration fee, bidder will get message for producing their Affidavit and system generated ID and class III digital certificate to nearest depot where the Authorized depot user will upload their affidavit in their account and will retain the original copy of affidavit. After Sign and Submit by Bidder he will be registered successfully .Bidder will receive in his mailbox Login Password to log into the application and the Bidding Password for participating and bidding in auctions. User ID will be same as his email ID given in the form at the time of registration.

Q.273 (a) How can Depot User create Auction Catalogue in E-Auction ?

(b) What is the procedure for Editing, deleting, rearranging, withdrawn lots in E-Auction?

Ans. (a) Auction Catalogue can be created by clicking the link available on left navigation of user home page ‘Create Auction catalogue’. There are 3 steps for making a catalogue.

1. Header Creation and Blocking of Bidders.

In Header Creation, the Auction Type whether Close Ended or Open Ended is defined and according to which the Max Auto Extension is given. The Auction start Date Time is automatically taken from the Auction Schedule. Depot Admin has also been given facility to block bidders. In Lot Finalization step, depot user can add lots to auction catalogue. Lots newly created after publishing of last catalogue, lots rejected/withdrawn from last catalogue are automatically included in next catalogue. He can add more Lots by clicking the button “Show Lots Not Included in Current Catalogue”. He can also remove lots by selecting the lots and remove them. In the Sequencing, the Depot user can arrange the lots and categories in catalogue in the desired order for auctioning. After catalogue is finally prepared, it can be published by using digital Signature Certificate. It is important to note that sequence of category and Lots cannot be changed after publishing a catalogue.

Ans. (b). During catalogue creation process, authorized Railway users can edit any details except Lot Number of any lot by clicking icon Edit Lot. Lot can also be edited by searching the lot from search facility. Lot can be deleted by searching the lot from search facility. Lot once deleted will not be available to user for inclusion in future catalogues. Lots which have already been sold cannot be edited/ deleted. Lots where Auction for the catalogue has started cannot be edited. During catalogue creation process, authorized Railway users can remove desired lots from catalogues. Such removed lots will be available for inclusion in the subject catalogue before start of Auction or for inclusion in any future catalogue.

Q.274 (a) Who can Enter/Edit/View RP for the lots in E-Auction & how?

(b) How can Railway User register the Bidder manually for E-auction?